Is the student party over? That’s a question the purpose-built student accommodation (PBSA) sector might not want to hear, given the likely answer.

Oli Creasey, head of property research at Quilter Cheviot, has been bearish on PBSA for almost a year and recent news has given him no cause to change his assessment. “Student accommodation has been a darling for a little while,” he says. “We’ve been given pretty tight valuation yields for quite a long time and been told you can still buy PBSA because the rental growth story is so strong. [But] that’s massively unwinding now.”

He cites the sharp fall in the stock market price of the sector’s biggest player, Unite Group, which has dropped by a third over the past year. As a result, its dividend yield has steadily grown – to around 7.5% at the time of writing.

“That dividend might actually be under threat,” Creasey says. “Pricing in student accommodation is now behaving a lot more like commercial property, more like the offices around it. I’ve been warning of this since the second quarter of last year and now quite a lot of people are questioning whether PBSA is just in for a couple of bad quarters – or is this now going to turn into a couple of bad years?”

Not surprisingly, Unite Group has a different view of its prospects. PBSA “remains fundamental to the UK’s world-renowned higher education sector and to the towns and cities it supports”, according to a Unite Group spokesperson. “A record number of UCAS applications in the latest cycle shows that student demand remains strong, with growth concentrated at the UK’s high-tariff universities.”

There’s probably just half a dozen cities where development is viable

Lizzie Beagley, Savills

The spokesperson adds: “Our long-term growth strategy and development pipeline are aligned to these leading universities and the cities where student housing is most constrained.”

Lizzie Beagley, head of transactions for PBSA and co-living at Savills, is among the sceptics when it comes to PBSA. “I do think a peak has been reached,” she says. “If you’re looking at it from a development perspective, it’s way harder than we’ve ever had it before, and we wouldn’t necessarily recommend to developer clients that they can go and build [PBSA] wherever they fancy anymore. Absolutely not.”

Few viable locations

She adds: “There are a few key locations where we see development being viable. We used to do a league table of where we’d recommend developers look at building new student kit, but the table got smaller and smaller until we stopped doing it.

“Now there’s probably just half a dozen cities where development is viable from a demand and supply perspective, and from a rents and yields perspective, in terms of having enough value per unit to cover costs.”

Beagley, among others, suggests that the few remaining viable PBSA locations are London, Oxford, Cambridge, Manchester, Bristol and Edinburgh.

Russ Mould, investment director at AJ Bell, notes that shares in Unite Group as well as student accommodation developers such as Watkin Jones have been in the doldrums for some time “thanks to the well-documented challenges that could crimp university attendance going forward”.

Those challenges include “a cooler welcome to overseas students, especially those from Russia or China”.

He adds that overseas students typically paid high fees, often as graduate students. “Their absence will be keenly felt from a financial point of view by universities and property developers alike,” Mould explains. “Some universities are already taking evasive action to cut costs, notably through the cancellation of some courses and curricula.”

PBSA is also likely to feel the impact of public debates about the high cost of student loans, the benefits of obtaining a degree, the rumpus around higher-interest Plan 2 loans – which Conservative leader Kemi Badenoch has said her party would cap – and the freeze on income tax thresholds bringing more graduates within the repayment threshold.

Mould says these debates “may encourage some to reconsider university and perhaps go down the apprenticeship path or seek a direct move into paid employment”.

According to Stacy Eden, partner and national head of real estate at business advisory giant RSM UK, PBSA has fallen out of favour as an asset class with investors over the past two years, primarily due to lower volumes of international students.

“Our recent Real Estate 360 survey demonstrates that only 12% of real estate business leaders view student housing as the asset class that will see the most growth over the next year, compared with 24% in 2023,” she says.

“This correlates with recent government data, which shows that last September, the number of student visas granted was 31% lower than in 2023, when student visas reached their peak.”

While many investors and analysts have become PBSA bears, some bulls remain. Shivani Goolab, head of private client lending at Investec Real Estate, continues to back the sector. Asked if PBSA development has peaked, she says “absolutely not” and adds: “July to September last year marked the largest third quarter on record for UK PBSA investment volumes, with £1.83bn changing hands. The sector has matured markedly over the past few years and while it has become more nuanced, it remains an attractive target for both domestic and international equity and debt capital.”

But Goolab does recognise the challenges faced by investors and developers alike. “UK university finances have come under increasing pressure,” she says, adding that the slowdown in international student numbers and freeze in domestic tuition fees have “created a more bifurcated market”.

As a result, she says investors are looking more closely at individual locations and universities, particularly those lower-tariff colleges hardest hit in recent years. She adds: “The Russell Group universities continue to perform well.”

Goolab says lower leasing velocity and reduced occupancy levels in some locations have required a more active asset management approach from operators to maintain income levels. For some less established operators, this has been a challenge. Rental growth has also moderated over the past academic year, albeit from a few years of outsized levels.

Robust investment case

Jessica Hardman, chief executive and co-founder of Aboria Capital, is also relatively upbeat about the PBSA market. “It would be premature to suggest it has even nearly peaked,” she says. “While parts of the higher education sector are facing financial pressures, the investment case for PBSA remains robust and underpinned by strong structural fundamentals.

“The latest admissions cycle saw record applications from UK school leavers and continued strength in international postgraduate demand, particularly targeting the UK’s globally leading institutions.”

Indeed, Hardman argues that the sector continues to be undersupplied, citing CBRE figures indicating a UK shortfall of more than 580,000 student beds.

Meanwhile, Max Bielby, chief operating officer at upmarket student accommodation developer and operator Vita Group, gives a more nuanced assessment. “I certainly agree that we’ve hit a threshold where the market is evolving and entering a new phase,” he concedes. “I think the fundamental point is that it feels like a flight to quality.

“I think people are seriously looking at the cost of a degree and really trying to weigh up whether it is benefiting their careers in the future [and] those who are doubling down on quality education, quality degrees and quality institutions are continuing to do so. [As a result] our investment thesis is to double down even more on alignment to the Russell Group universities.”

Vita Group focuses on the top university cities listed by Savills’ Beagley and targets the lucrative overseas student market in particular. A whopping 85% of its beds are taken up by foreign students, who are offered a breadth of facilities ranging from personal chefs to private cinemas, which allows it to charge significantly more than less rarefied rivals.

“There are seven million students globally who partake in tertiary education outside their home country,” Bielby says. “The UK currently attracts about 10% of that global market share – about 700,000 international students.

“These international students come to the UK and pay £38,000 to £40,000 in fees alone. So, when their families have invested that much in fees, they don’t view spending a bit more on their accommodation as a problem.”

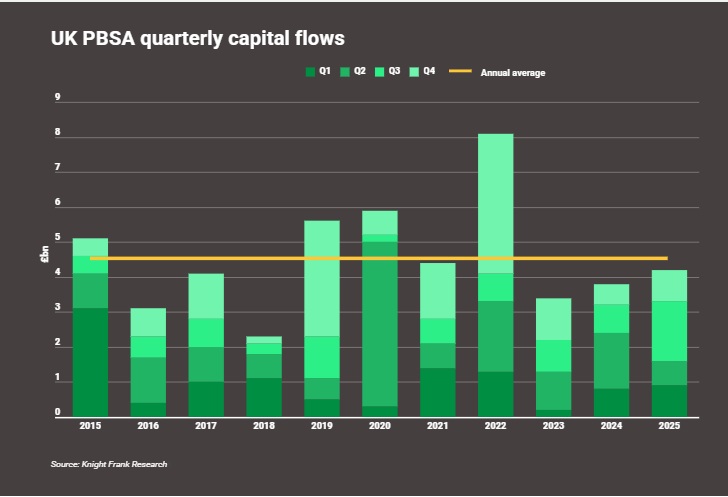

Knight Frank reports rise in beds despite tough development landscape

UK PBSA quarterly capital flows Infogram

The Q4 2025 UK Student Market Update report from Knight Frank, published last month, records 19,600 new PBSA beds added to the market across 64 schemes in 2025, up 20% on the previous year.

In total, £4.3bn was invested in new PBSA developments in 2025, a 10% increase on the prior year and close to the £4.5bn 10-year average for the sector.

“A tougher development landscape – with significant delays at the Building Safety Regulator because of gateway 2, alongside planning and viability challenges – has had an impact on capital allocation,” the report notes.

It adds that around 40% of existing PBSA beds are controlled by just nine investors, while the rest is “fragmented and fiercely competitive for scale”.

Knight Frank says that this year, capital is likely to be deployed to expand and reshape portfolios, with growing interest in Russell Group locations, mid-scale buildings of 400 to 500 beds and middle-market assets that bring in both domestic and international students. It also predicts more active asset management as a route to higher rents.

Follow us on LinkedIn

Follow us on LinkedIn